Always procrastinating and think that there will be a better time down the road, whereby you make more money before investing? You will be dead wrong.

Waiting to invest is one of the biggest mistakes that you will be making in your young adult years because you will be throwing away so much valuable time in the markets. Investing early enables you to not only take advantage of using the time to mitigate fluctuates in the market, but also allows you to benefit from compound interest.

Compound interest is the addition of interest to the principal (or initial sum of money) that you first deposited. When the interest you receive from your investments generates even more interest, that money is compounded and keeps multiplying on and on.

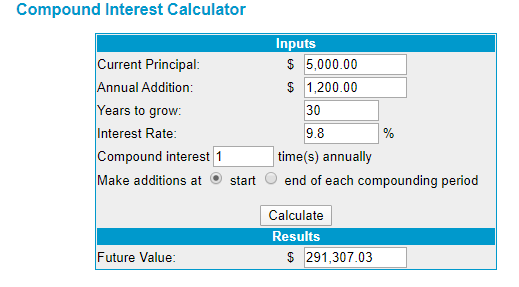

Imagine this, if you started with an initial investment of $5000 and add $100 every month for the next 30 years (whereby you will be around 50 years old) into the SP500 index fund. Assuming that the SP500 generates the same annual return as it has over the past 90 years of an average 9.8% per annum, you will be having $291,307 by the time you are 50!

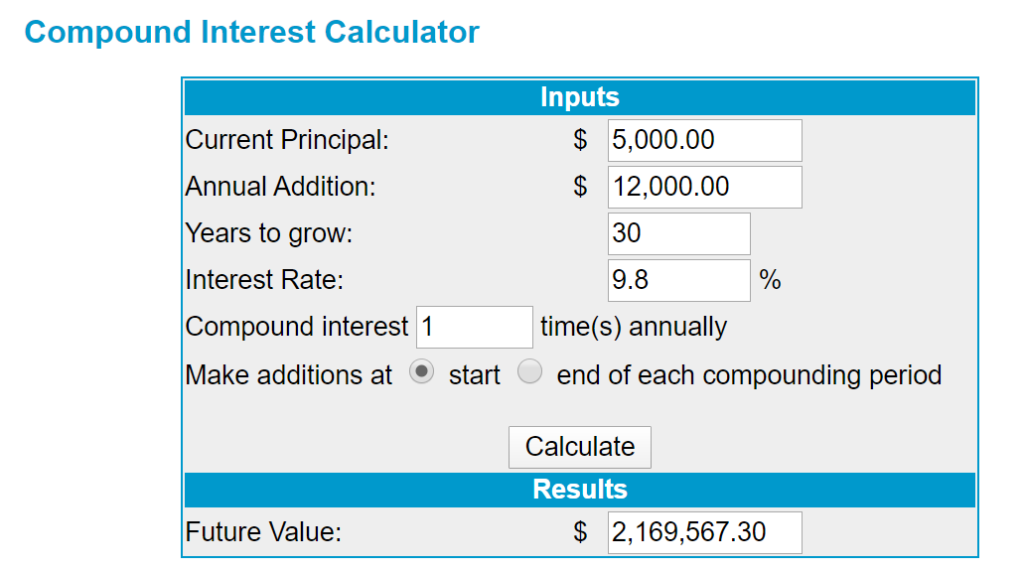

Now, if you are truly serious about investing and instead invest an average of $1000 per month for the rest of the next 30 years (Take note that it is an average of $1000 which probably means you invest less at the start of your career and more at the later periods where you make the bigger bucks), let’s see how much you would have saved!

No, there is certainly not any camera trickery here, calculate it for yourself! You would have saved a whopping $2,169,567, over 2 million dollars! Imagine the number of real estate properties you could own by the time you are 50, and enjoying the joy of collecting rent and capital gains from the appreciation of property prices at that age! Retirement could come early if you plan your investments wisely, assuming that stock markets continue to behave as they always have.

While not everyone may be fortunate enough to set aside a $1000 per month, you can always determine your own investment goals using the compound interest calculator by moneychimp.

As you progress through the different levels and echelons of your career, you will start to come up with all sort of reasons to justify the purchase of several things that plague your bank account:

Seriously, take public transportation if the place that you live in has a reliable one. If not, go for used or secondhand cars. After all, all you need is a vehicle to get from point A to point B and brand new cars will come in when you are in a better position financially. Right now, there should not be any talk about getting a brand new Toyota, let alone a Tesla.

Unless you are sure that the benefits from owning a brand new car justify the costs associated with it, especially if you are in sales, or else postpone buying a new car.

Some might say to dress like the job you want to be. But do you want to be working forever or retire early? Spend on affordable brands and create a flexible wardrobe suitable for every occasion but not looking like you are incredibly cheap. Avoid luxury brands at all costs in your early adult years.

Starbucks, Coffee bean, whatever coffee you find in stores can also be made at home at a fraction of the price. You will be surprised by how much money you can save by making your own coffee that you otherwise deem as a necessary expense to sustain your energy at work.

These are some of the items that can absolutely destroy bank account, so avoid spending money on these and you will be surprised how much that savings can be channelled into your investments that will accrue and compound over the years.

If you fail to plan, you plan to fail. Most people that you meet across your life are more than likely not to follow a strict budget. Honestly, how many people do you know actually track their finances to the dollar? Most people have a vague idea of how much they spend based on their account balance, but they do not know precisely how much is spent.

To save successfully in your 20s so that you can enjoy in the future, make sure that you record down your expenses and continually track them so that you know if you are spending too much money.

There are tons of budgeting applications that can help you with this, including Mint or Wally, which are guaranteed to help you better.

If you need to keep track of who owes you or who you owe money to, then Splitwise is the solution for you.

At the end of the day, it is still your life decision that you have to make. Would you want to spend now but still have to work for money in your 50s? Or invest now, live below your means and spend your golden years at the beach chilling.

Related: